{kind=link}

This is the most comprehensive step-by-step approach for applying and attaining Mortgages in Dubai.

Let’s get started.

What is a Mortgage?

In short, A mortgage is a type of loan you obtain to pay the value of a property.

Generally, a mortgage for your residential property is called a home loan.

Commercial properties can include warehouses, office spaces and other properties used for commercial purposes.

When it comes to mortgage in Dubai, most procedures are similar to conventional banking; however, a few key factors do change.

So, you need to understand each aspect of finding and getting a mortgage for your property in Dubai.

[lwptoc]

Summary of Best Mortgages in Dubai 2023

| BANK | RATE OF INTEREST (Starting from) | MINIMUM SALARY | LOAN AMOUNT (MAX) |

|---|---|---|---|

| Standard Chartered Mortgage One | 4.39% (reducing) | 15000 AED | 18 Million AED |

| RAKBANK Home in One | 4.39% (reducing) | 15000 AED | 20 Million AED |

| CBD Mortgage Loan for Expats | 3.99% (reducing) | 15000 AED (Salaried people); 20000 AED (Self-employed) | 10 Million AED |

| Emirates NBD Home Loan for Expats | 3.99% (reducing) | 15000 AED | 15 Million AED |

| Standard Chartered Home Suite | 4.29% (reducing) | 15000 AED | 18 Million AED |

| ADIB Home Finance for Expats | 3.99% | 15000 AED | 15 Million AED |

Getting a Mortgage in Dubai

If you decide to purchase a property in the UAE, the best-suggested destinations are Dubai and Abu Dhabi.

Between the two, Dubai is most popular for the availability of top-notch residential and commercial spaces.

The cost of these properties can seem a pressure on your current financial state. But don’t worry! You can get a mortgage to purchase your very new office or a new place to live in.

To successfully complete the process of getting a mortgage, you should understand all about the eligibility criteria, according to the guidelines of the UAE Central Bank.

UAE Nationals and Expats have to complete different eligibility criteria provided by the UAE Central Bank. In our previous blog, we covered about expat’s guide to buying a property in UAE.Â

An LTV value, which is also known as Loan to Value, is an overall loan value you get with respect to the property price.

There was a time before 2008 economic depression when candidates applied and obtained loans with very low and convenient down payments. This requirement used to go down to 5 percent as well. But the post-depression period got introduced with new guidelines regarding mortgages and their down payments.

Down payment for a mortgage in Dubai

There are no exceptions when it comes to current down payment guidelines provided by the Central Bank in UAE.

All applicants have to contribute a payment portion.

Maximum LTV or Loan to Value to purchase a ready property:

For expatriates who want to purchase ready properties-

- If the property value is 5 million in AED or below, the LTV stands 75%.

- If the property value is more than 5 million in AED, the LTV stands 65%.

- If you are buying a second investment property or a home, the LTV stands about 60%.

For example, a bank can offer about AED 750,000 for a property with 1 million value in AED, depending on eligibility.

Similarly, a bank can offer about 3.25 million in AED for a property with 5 million price value in AED, depending on the eligibility.

For UAE nationals who want to purchase ready properties-

- If the property value is 5 million in AED or below, the LTV stands 80%.

- If the property value is more than 5 million in AED, the LTV stands 70%.

- If you are buying a second investment property or a home, the LTV stands about 65%.

- These LTV values are applicable to freehold as well as leasehold ready properties.

Maximum LTV or Loan to Value to purchase an off-plan property:

The off-plan properties have the same 50% of maximum LTV for both UAE nationals as well as expats.

A step-by-step approach to applying and attaining a mortgage in Dubai

At a single glance, applying and attaining a mortgage can seem daunting. But you can divide the process into different smaller steps and reduce stress.

Here is how you can do it:

Step #1: Choose your property

There are many platforms online to find properties in the UAE. You can select a few of many reputed sites to check their property listings.

With the lists of properties, you will gain different options of ready properties and off-plan properties.

However, ready properties are more popular among buyers. This way, a home or an office comes with all facilities and developments.

So, you can move right away to utilize the property or get immediate rent. This allows you to start getting an appreciation of your invested capital.

At the same time, bank guidelines are stricter when it comes to off-plan property mortgage.

Step #2: Get an agreement from the property seller

You can either purchase directly from a property developer or utilize the secondary market. In case of direct purchase, you need to get the sale contract from the developer.

To ease the process, you should consider a licensed broker or a reputed real estate agency to complete the property transaction.

In any case, your involvement in the contract creation matters the most. Know your rights and go through the contract with some help from a professional.

Sellers try to negotiate a higher down payment. You should take the help of your real estate broker or consultant

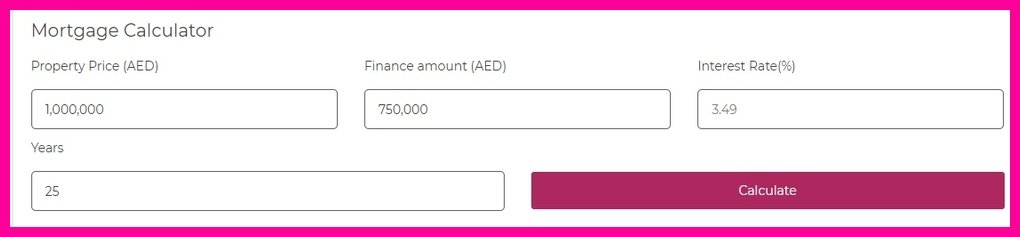

Step #3: Calculate mortgage using Mortgage Calculator and find a list of best-suited mortgage options

After you have an agreement regarding the purchase price of the selected property, it is time to calculate mortgage.

You can use the Mortgage Calculator provided by Compare4Benefit. The calculator makes mortgage calculation a simple task:

Provide mortgage-related information

You already have your property price in AED.

Include that in the calculator along with the Finance amount you desire, the interest rate you expect and the years of repayment.

After entering all the required information, you can calculate your mortgage with a single push of a button.

The results provide mortgage repayment associated details.

The results provide mortgage repayment associated details.

The tool also provides information about approximate bank charges as well as the charges required for the land department in UAE.

The calculator shows an amount you will have to pay with respect to the details you enter. This amount has to be convenient as per your financial condition.

Using the results of mortgage calculation, you can obtain a list of best-suited mortgage options available in UAE.

Compare4Benefit shows mortgage products with details regarding maximum terms, interest rate, required salary and more.

Step #4: Collect and review all the required documents

You can get professional mortgage assistance to review your documents. A professional ensures that you collect all the required documents.

This step is critically important to avoid unwanted delays during the approval process conducted by the bank.

Documents Requirement For a Salaried Employee:

- A copy of a valid passport.

- Expatriates need a valid visa.

- A valid Emirates identification.

- Latest salary certificate.

- Bank statements with salary credits for the latest 6 months.

- Disclosure of every monthly liability such as a car loan, credit card, personal loan, etc.

- Six-month payslips in case if there is salary variance.

- Availability of fees required for mortgage processing.

- Down payment proof

Documents’ requirement for a self-employed:

- A copy of a valid passport.

- Expatriates should present a valid visa.

- A valid Emirates identification.

- Trade License Copy

- MOA or Memorandum of Association, plus, incorporation documents.

- Audited financials of previous 2 years (Not a compulsory requirement by all banks).

- Six-month company bank statement.

- Six-month personal bank statement.

-

Disclosure of any company monthly liability such as a business loan,auto loan, company facility, etc.

- Disclosure of any monthly liability such as a car loan, credit card, personal loan, or others.

- Some sale-purchase invoices.

- Mortgage pre-approval fees.

- Down payment proof.

Along with all this, you should collect property associated documents such as the agreement (MOU) and title deed. Property documents can be submitted to the bank after pre-approval

The documentation requirement can increase depending on the guidelines followed by the selected financial institution for a mortgage.

Step #5: Submit your documents

You can fill the form on the top to finalize the bank for your Mortgage requirement by taking assistance from the Mortgage representative.

You need to fill the bank forms and provide your documents along with them.

Your mortgage representative or you can submit the forms and the required documents to the bank authorities.

Then, the bank authorities review all the submitted documents.

This is the time when you can present your request to obtain a pre-approval.

When it comes to deciding your eligibility, banks follow the same approach as for a personal loan.

The Debt to Burden Ratio or DBR is calculated with respect to your financial condition and the asked loan amount.

Step #6: Get the pre-approval issued from your mortgage provider

Bank authorities review documents along with the clarifications you provide. This leads to the process of getting a pre-approval from the bank.

This is a letter, which includes the name of the applicant along with the amount of loan approved by the bank.

Along with that, the pre-approval letter also shows tenure of the loan and the interest rate. You can see the conditions written in this letter that help in obtaining the final approval successfully.

The validity of a pre-approval letter lasts for 30 to 90 days. The exact time period depends on the guidelines followed by the selected bank or a financial institution.

A few banks ask some fee to provide a pre-approval letter.

Step #7: Ensure property identification

Property identification is the process of inspection before the purchase procedure begins. You need to make sure that you are protected in terms of the commitments made to the mortgage finance provider.

This requires getting copies of title deed, floor plan, contracts and other documents to strengthen your position as a buyer.

Step #8: Wait for Property Evaluation

At this stage, the bank asks you to pay property valuation fees which ranges between AED 2500 and AED 3000 along with taxes.

Bank hires a third-party evaluator to complete the property valuation and submit the valuation report.

The evaluator company can take up to 3 consequent working days after the property inspection to provide its valuation report to the bank.

Step #9: Obtain an Offer Letter

When the bank receives the valuation report, the final offer is initiated.

This is the phase when all the conditions presented in the pre-approval are fulfilled to get the offer approval.

The bank sends you a letter approving its final offer. You and your mortgage representative can review the letter.

Only after thoroughly inspecting and accepting the offer letter, you should sign all the documentation provided by the bank.

Step #10: Go through a medical check-up

Life insurance is compulsory with most of the banks equivalent to the Mortgage amount. In some cases, insurance companies can advise you to go through some medical check-ups (which is mostly advised in case of higher finance amount or in the case of the elderly age client).

Step #11: Fulfill the request for a certificate of no objection

First of all, get all the signed documents and property-related documents in order. The bank asks for a developer NOC or No Objection Certificate from the buyer (if its applicable).

If you are dealing with real estate brokers, they take care of arranging this letter.

Step #12: Complete the property transfer

![]()

A representative from the bank schedules the property transfer.

The process takes place at one of many Land Department trustee offices in Dubai.

Some transfer processes take place at the respective developer office.

Step #13: Receive documents and the key

It is Land Department’s responsibility to provide you with a Title Deed.

The Title Deed should have your name as the property owner. Plus, the bank is represented as your mortgage provider.

The lender of the mortgage becomes the property owner if you select an Islamic Finance and you become the lessee.

You only receive a copy of the prepared Title Deed, as the original Title deed is received by the lender bank. Plus, you receive a key of the property from the seller.

After completing the last step, your mortgage becomes effective right away. So, your installments begin, which you need to pay every month.

What should be the expected interest rate or profit rate for a mortgage in Dubai?

Home loans are considered secure among other types of loans, which is why you get lower interest rates for the mortgage.

Usually, the interest or profit rate stays around 2.99 to 7 percent. This range of percentages makes negotiation a necessity for you.

The rate of interest should go down as much as possible. Even if you get a tiny discount, it creates a big impact on your overall mortgage.

You should look at the big picture here and calculate the benefits of a reduced interest rate with respect to the loan period.

How long can it take to get a mortgage approved?

These days, lenders don’t waste too much time. There are more efficient ways to conduct and complete required assessments.

Generally, a salaried employee has to wait for 7 working days to get the mortgage approved.

However, the approval of mortgage for a self-employed individual can take a longer time period.

How to ensure the protection of assets?

In certain cases, lenders ask to get life insurance from them against the amount of mortgage.

The insurance providers are offered by the lenders. This allows you to keep your assets protected, in case of your sudden death.

But to get this protection, you will have to pay an insurance premium along with your monthly mortgage installments.

Does pre-approval matter?

Pre-approval is always a good choice to guarantee your eligibility and safeguard your final approval of the mortgage.

Imagine a situation when you pay your down payment to the seller, but then, the bank rejects your mortgage application. No one wants that.

How does the Islamic home mortgage work?

Islamic home mortgage works in compliance with Shariah banking.

Most individuals in the Muslim community prefer this mortgage approach.

The Shariah banking doesn’t ask for interest for the home finance. Also, the finance structure differs from the regular mortgage structure.

In Shariah banking, the roles of lender and borrower turn into Lessor-Lessee. The finance institution works as your lessor, while you borrow mortgage as a lessee.

Monthly installments are called rent and the finance provider operates as the property owner until you pay the whole mortgage back.

The property registration process at the Land Department Dubai

The property registration in Dubai is possible at one of many Land Department trustee offices. Registration is necessary to generate evidence of owning a property.

According to Article 22 in the applicable law, the Land Department ensures the rights of real property by providing the title deed.

The title deeds are provided according to the records available currently in the registers of real properties.

- The New Law Article 6 gives property registration rights to the Land Department only. This registration authorization includes leases for long terms and property rights altogether.

- You, as the purchaser, can sign the transfer form provided by the Land Department. This transfer form is used internally in the department.

The process of property registration is chargeable. The buyer has to pay a 4% charge to the Land Department (2% in case of Abu Dhabi property).

Why should you compare different mortgage options?

Mortgage comparison in UAE is a wise move, as there are many options available. You can choose the best-suited mortgage option by comparing the interest rates, tenure, and other features.

What are the hidden costs to consider when looking for a mortgage in Dubai?

When a new home is your ultimate goal, you easily get emotional and make mistakes in terms of money.

Home buying, if requires a mortgage, you need to have a rational approach. You have already read the different steps required for mortgage approval.

And all those steps can present with sudden expenses, which you should be aware of.

- Application, documentation, and processing fee

The mortgage provider can ask fees in different ways for the documentation, application, and processing as well. The fee amount can range from 0.25 percent to 1 percent with Vat. Some lenders can even go beyond those percentages. You have to have a clear talk regarding the processing and other fee associated with the procedure. Ask your lender if they charge fees for pre-approval and/or any other process.

- Valuation fees

The valuation fees are asked by the bank, which reaches a valuation company. This company provides valuation report regarding the property. The valuation authorities can ask for an amount AED 2500. However, it is possible that the bank adds a margin and asks you to pay up to AED 3,000.

- Bounced cheque charge

If any installment cheque bounces, you become liable to pay an additional charge.

- Pre-pay charges

In case you successfully pay your loan early, it damages the expected interest. So, the bank charges a penalty for pre-pay to recover the losses.

Some banks give a benefit of free partial settlement up to some percentage.

- Loan transfer charge

You can transfer your loan from one provider to another in the middle of your tenure. However, this facility comes with additional fees. The bank or the lender will charge you a fee. Plus, you will have to pay an additional amount of money to the Land Department as well.

Buying your dream home or office in Dubai is possible now! You just need to understand the mortgage process thoroughly and utilize a Mortgage Calculator to find the best-suited loan features. This way, you can secure your financial situation and purchase a property you desire.

For a smooth completion of the process, you should surround yourself with qualified professionals. At the same time, don’t forget to improve your property and mortgage knowledge to make smart decisions.

Who can apply for a mortgage?

An individual working as an employee in UAE can apply for a mortgage. Also, a businessman or any other self-employed person can also apply using the available financial institutions.

Non-residents have to follow different guidelines, but they can also use the available mortgage facilities in Dubai. The eligibility criteria can differ for such candidates.